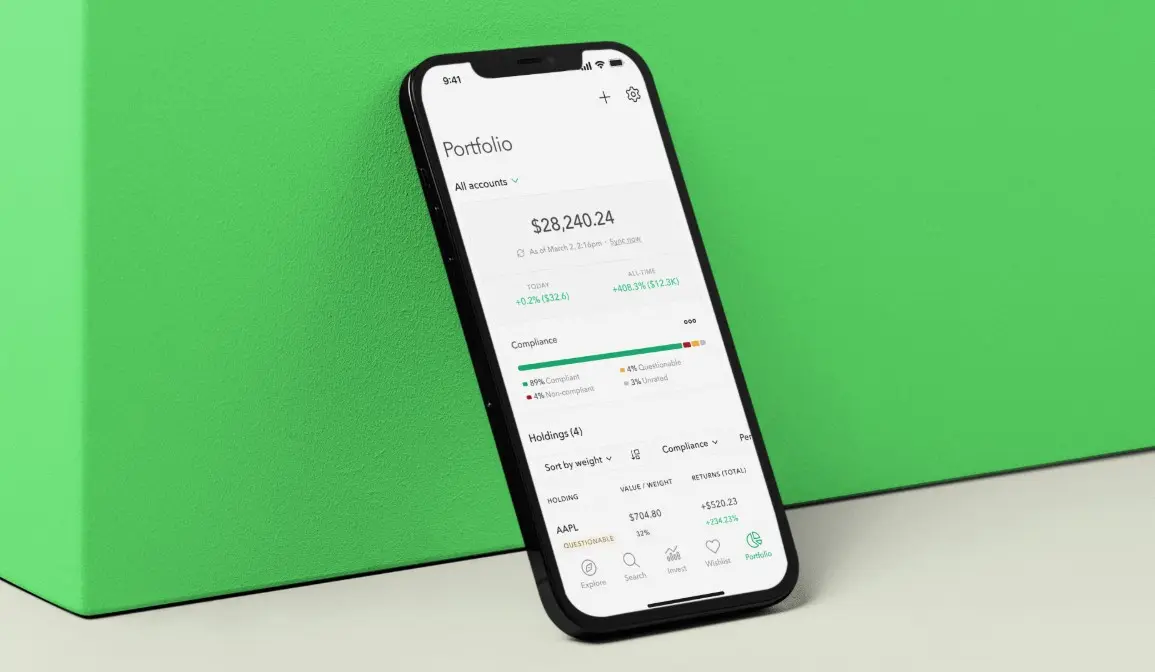

Getting started with Halal investing is a great first step, but creating a portfolio that really fits your personal situation takes a bit more thought. Many people follow generic advice and end up with investments that don’t quite match their real needs or goals. Your financial journey is unique—your age, family situation, income, and dreams for the future aren’t exactly like anyone else’s. That’s why customizing your Halal investment portfolio matters so much. When your investments align not just with Islamic principles but also with your personal circumstances, you’re more likely to stick with your plan through market ups and downs. The good news is that today’s Halal investment world offers plenty of options to tailor your approach while staying true to your values. Let’s customize your Halal investment portfolio.

Tip 1: Match Your Investments to Your Life Stage

Your age and life situation should drive your investment choices—what works for a 25-year-old won’t make sense for someone nearing retirement. If you’re young with decades ahead, you can handle more ups and downs in the market, so consider putting more money in Shariah-compliant stocks or equity funds. These might bounce around more in value, but historically they’ve grown more over long periods. I’ve seen young investors do well with 70-80% of their money in Islamic equity funds and the rest in safer options like Sukuk. But if you’re getting closer to retirement, you might flip that mix—maybe 60-70% in steady Sukuk investments and less in stocks. The same goes for major life events—getting married, having kids, or buying a home might mean adjusting your mix to have more stable, accessible investments for a while. Remember, your investment strategy should change as your life changes.

Tip 2: Consider Your Comfort With Market Swings

Some people can sleep just fine when their investments drop 20% in a month, while others lie awake worrying when they drop just 5%. There’s no right or wrong here—it’s about knowing yourself. Try this simple test: think back to market drops in the past (like March 2020 when COVID hit). How did you feel? Did you panic and want to sell everything? Or did you stay calm or even get excited about buying more at lower prices? Be honest with yourself! If market drops make you extremely anxious, build a more conservative Halal portfolio with more Sukuk and Islamic fixed income options, even if you’re younger. On the flip side, if you’ve got the stomach for ups and downs and a long time horizon, you might choose more Islamic equity funds. Your faith in the market’s long-term growth needs to match your emotional ability to handle the rocky parts of the journey.

Tip 3: Align Investments With Your Personal Values Beyond Halal

Halal investing already avoids industries like alcohol and gambling, but you might have additional values you care about. Maybe environmental issues matter deeply to you, or perhaps you’re passionate about healthcare advancements. The good news is you can find Shariah-compliant investments that also support these values. For example, there are now Islamic ESG funds (Environmental, Social, and Governance) that focus on companies making positive impacts while still following Islamic finance principles. Or you might look into Islamic healthcare technology funds if that sector matters to you. I recently spoke with a client who cares deeply about clean energy—we found several Shariah-compliant renewable energy companies that fit both his Islamic requirements and environmental concerns. These “values within values” investments often feel more meaningful and can make you more committed to your long-term plan.

Tip 4: Factor In Your Local Economy and Currency

Where you live affects how you should structure your Halal portfolio. If you’re in Malaysia, Indonesia, Saudi Arabia, or the UAE, you’ll have different local Shariah-compliant options than someone in the US, UK, or Canada. Think about your daily expenses, too—what currency do you spend in? It often makes sense to keep a good portion of your investments in the same currency you use for everyday life. But not all of it! Having some investments in other strong currencies can protect you if your local currency weakens. For example, if you live in Egypt and all your investments are in Egyptian pounds, you might consider adding some Sukuk denominated in US dollars or Gulf currencies. I’ve worked with families who live in one country but plan to move to another in the future—their portfolios include Halal investments from both regions to smooth the transition. Your portfolio should reflect both your current reality and your future plans.

Tip 5: Create “Buckets” for Different Financial Goals

Instead of thinking about your Halal investments as one big pot, try dividing them into separate buckets for different goals with different timelines. Maybe you need money for Hajj in two years, for your children’s education in ten years, and for retirement in thirty years. Each of these goals deserves its own investment approach. For your Hajj fund, which you’ll need soon, stick with very stable options like Shariah-compliant money market funds or short-term Sukuk. For education funds, a mix of Sukuk and stable Islamic equity funds might work well. And for retirement decades away, you can consider a more growth-focused approach with Islamic ETFs and funds that invest globally. Many investment platforms now let you label accounts for specific purposes, making this bucket strategy easier to manage. I’ve found this approach helps people resist the temptation to tap into long-term investments for short-term needs, which is one of the biggest mistakes investors make.

Also Read-Car Floor Mats Online: How to Find the Best Deals and Quality Mats for Your Vehicle